The New Retirement Risk: Outliving Your Portfolio

6/3/2026

Years ago, the largest threat to retirement planning was market volatility. What if the market experienced a notable dip and your portfolio followed suit? Today, though, there’s another – and potentially more serious – factor to plan for: People are living longer than ever, and now, they need to ensure their retirement assets last just as long.

Between 1960 and 2015, life expectancy in the U.S. increased by almost 10 years – from 69.7 to 79.4. And by 2060, it’s projected to increase to 85.6.1 With the right planning, your investment strategy can evolve to support a longer life – balancing long‑term growth, income and healthcare needs so you can feel secure through every stage of retirement.

The Risk: Playing It Safe Too Soon

It’s not uncommon for investors to begin dialing back investment risk in their late 50s or early 60s, often shifting more of their portfolio toward cash or bonds. Today, however, that shift toward lower‑risk assets can increase the risk of outliving your savings. By limiting growth, you reduce your portfolio’s ability to keep pace with inflation and rising healthcare costs.

Over time, even mild inflation can slowly reduce the value of your money. A portfolio of bonds or money market funds that is focused mostly on short‑term stability may struggle to keep up with rising costs over a longer retirement. Increasingly, an approach designed to reduce your uncertainty today can create larger challenges later if growth doesn’t keep pace with your living expenses.

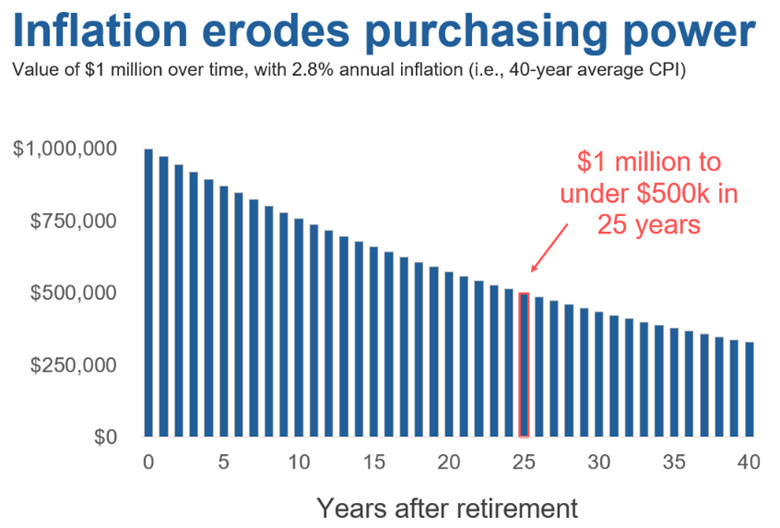

To see how this plays out over time, consider the chart below. It shows the value of a $1 million nest egg over the course of four decades, assuming constant inflation of 2.8% per year (i.e., the average inflation rate in the U.S. over the last 40 years). As you can see, after just 25 years, the value of the portfolio is cut in half.

Rethinking Time Horizon and Asset Allocation

But if you shouldn’t make an all‑or‑nothing move into “safer” investments as you approach retirement, what’s the right alternative? For many investors, the answer is a more gradual shift – one that balances stability for short‑term needs with growth for the future, rather than making sudden changes to their portfolio.

More stable investments, such as bonds or cash, can help support short‑term spending and remain steadier through market ups and downs. At the same time, growth‑oriented investments can handle more market exposure for a longer period of time – helping support longer‑term needs later in retirement. By adjusting your asset mix over time – and maintaining some growth throughout retirement – you can help your portfolio remain resilient as markets change and your personal needs shift.

This approach may be contrary to a common rule of thumb: that the percentage of your portfolio invested in stocks should be “100 minus your age.” Using this strategy, a 60‑year‑old might hold about 40% in stocks, with the rest in more conservative investments. Today, that thinking is changing, and “120 minus your age” may be more appropriate for some investors – allowing for continued growth potential over a longer retirement.

Even after updating your strategy, your portfolio mix is not a set‑it‑and‑forget-it decision. Regularly reviewing your allocations can help ensure your investments continue to support where you are now and where you’re headed.

How Spending Changes Throughout a Longer Retirement

Retirement spending rarely declines in a straight line. Instead, it often follows a horseshoe pattern – sometimes described as the go‑go, slow‑go and no‑go years. Early in retirement, spending may naturally be higher as you take advantage of good health to travel, pursue interests and enjoy experiences you may have postponed while working. In the middle years, your spending may fall to a slower pace as your activity dies down and your retirement routine settles. Later on, your expenses may rise again as healthcare needs – like in-home care or treatment plans – become more significant. Plus, healthcare costs tend to outpace general inflation, rising more than 120% since 2000 versus about 86% for overall prices.2

As each of these retirement phases begin to lengthen, many traditional withdrawal guidelines – built around a roughly 30‑year retirement – may need to adjust for longer lifespans. For example, the “4% rule,” which says you should withdraw 4% of your portfolio annually over a roughly 30-year retirement. Today, withdrawals closer to 3–3.5% may help improve sustainability. However, balance is key: Setting spending too low can also mean unnecessarily limiting your lifestyle in the early years. Flexible withdrawal strategies – adjusted over time based on markets, expenses and health – can help balance your long‑term security with the life you’ve envisioned for your golden years.

Building Flexibility Into Your Retirement Income Strategy

Preparing your investments to support a longer, more flexible retirement works best when combined with other planning strategies. For example, delaying Social Security can boost your guaranteed income later on, helping cover everyday expenses as your spending needs change over time. You may also choose to take advantage of annuities, which can provide steady, predictable income and help ease the impact of market ups and downs.

Having a plan for healthcare costs – and keeping some cash set aside for emergencies – can also make a big difference. These steps can help cover unexpected expenses without needing to tap investments at the wrong time. Combined with maintaining some growth in your portfolio and reviewing your plan regularly, this can create flexibility and confidence throughout retirement.

Integrating Health and Wealth During Your Retirement

As people are living longer, taking care of your health plays an increasingly important role in shaping your retirement. Health and finances are closely connected, even for those who feel well prepared financially. Good health can provide more flexibility around spending and withdrawals, allowing you to stay active, pursue interests and potentially manage medical costs more effectively in the early years. Investing time and resources in preventive care and healthy habits can help support both your quality of life and your wealth plan over a longer retirement.

At the same time, it’s important to recognize that health trajectories can change. Health challenges can bring higher medical expenses or require drawing on assets sooner than expected. Because these paths can look very different, retirement planning works best when it accounts for both possibilities. That includes building room in your plan for preventive and long‑term care costs, stress‑testing your strategy in both best‑case and more challenging scenarios and avoiding relying on working longer. By planning this way from the start, your investments can remain a steady support system regardless of how retirement unfolds.

Living longer is often a gift – but it also requires you to evolve your financial and healthcare strategies with greater intention. Our team can help you create a proactive, flexible plan that supports both your financial confidence and your well-being through every stage of retirement.

This information has been developed by a member of Baird Wealth Solutions Group, a team of wealth management specialists who provide support to Baird Financial Advisor teams. The information offered is provided to you for informational purposes only. Robert W. Baird & Co. Incorporated is not a legal or tax services provider and you are strongly encouraged to seek the advice of the appropriate professional advisors before taking any action. The information reflected on this page are Baird expert opinions today and are subject to change. The information provided here has not taken into consideration the investment goals or needs of any specific investor and investors should not make any investment decisions based solely on this information. Past performance is not a guarantee of future results. All investments have some level of risk, and investors have different time horizons, goals and risk tolerances, so speak to your Baird Financial Advisor before taking action.